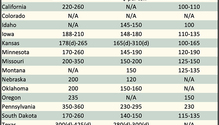

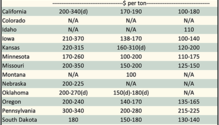

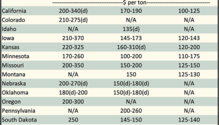

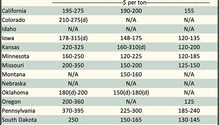

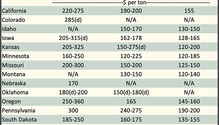

Below are examples of alfalfa and grass prices being paid FOB barn/stack (except for those noted as delivered, which are indicated by a "d" in the table below) for selected states at the end...

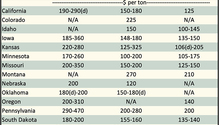

Below are examples of alfalfa and grass prices being paid FOB barn/stack (except for those noted as delivered, which are indicated by a "d" in the table below) for selected states at the end of...

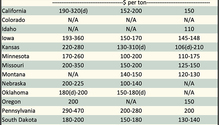

Below are examples of alfalfa and grass prices being paid FOB barn/stack (except for those noted as delivered, which are indicated by a "d" in the table below) for selected states at the end of th...

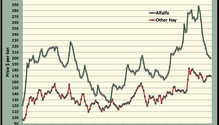

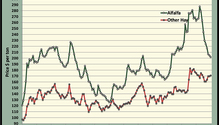

If the hay market was a hospital patient, the doctors and nurses would be on the run because the average price paid for hay has essentially flatlined. The February average price for alfalfa hay retrea...

Below are examples of alfalfa and grass prices being paid FOB barn/stack (except for those noted as delivered, which are indicated by a "d" in the table below) for selected states at the end of the...

Below are examples of alfalfa and grass prices being paid FOB barn/stack (except for those noted as delivered, which are indicated by a "d" in the table below) for selected states at the end of the...

Below are examples of alfalfa and grass prices being paid FOB barn/stack (except for those noted as delivered, which are indicated by a "d" in the table below) for selected states a...

Below are examples of alfalfa and grass prices being paid FOB barn/stack (except for those noted as delivered, which are indicated by a "d" in the table below) for selected state...

As the calendar turned to a new year, there wasn’t much new on the hay market front. The January average price for alfalfa hay retreated a modest $3 per ton from the previous month to $202, accordin...

Below are examples of alfalfa and grass prices being paid FOB barn/stack (except for those noted as delivered, which are indicated by a "d" in the table below) for selected states at the...