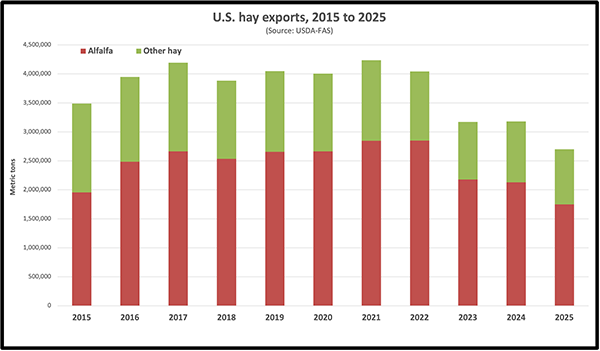

Hay exports in 2025 totaled 2.7 million metric tons (MT), according to USDA’s Foreign Agricultural Service (FAS). This was down 17% year-over-year, following a relatively flat trend the previous year. Trade disputes and steep exchange rates with our nation’s largest hay export markets had a significant impact on the reduced annual total.

China and Japan — the biggest consumers of U.S. alfalfa and grass hay, respectively — imported substantially less product in 2025. In fact, for the first time since 2020, total hay exports to Japan surpassed that for China, which speaks to the severity of China’s softened demand for U.S. alfalfa.

It’s not just China

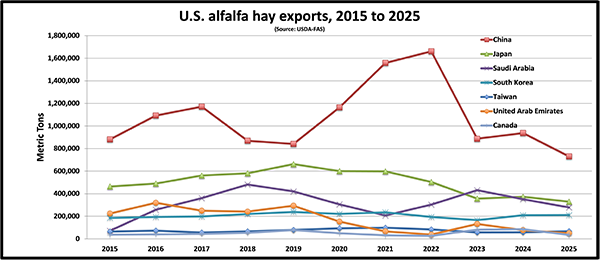

At 1.747 million MT, alfalfa exports to all trade partners in 2025 slid almost 20% from 2024. This was the third consecutive year-over-year decline in alfalfa hay exports since the record high of 2.847 million MT was set in 2022.

China imported 22% less U.S. alfalfa hay in 2025 compared to 2024, rounding out the year with 730,239 MT. This represented about 42% of total U.S. alfalfa hay exports, which was significantly less than the 57% majority market share that China claimed in 2022.

Last spring’s trade disputes with China took an obvious toll on its demand for alfalfa hay. From March to April, monthly volumes fell from 82,982 MT to 50,397 MT, down 39% month-over-month. That dropped to 24,190 MT in May, another 52% decline. Alfalfa hay exports rebounded in late summer and through the fall, but they did not come close to the monthly volumes normally delivered to China over the past few years.

Blaine Calaway, chief operations officer of Calaway Trading Inc. in Ellensburg, Wash., said that despite China’s recent dominance on the alfalfa hay export scene, it is considered an immature market. Alfalfa exports to China experienced unprecedented growth between 2009 and 2022 when totals peaked at 1.4 million MT and accounted for the majority of alfalfa leaving U.S. ports. Since then, China’s dairy industry has been deteriorating, which has inherently driven demand for alfalfa hay lower.

Japan maintained second place on the alfalfa hay export podium with a total of 329,559 MT in 2025. However, this was down approximately 13% year-over-year. Saudi Arabia was the third-largest export market for alfalfa hay with 277,987 MT in 2025, down 30% from 2024.

Alfalfa hay exports to South Korea were relatively steady year-over-year at 210,746 MT, maintaining fourth place. Taiwan and the United Arab Emirates trailed with 66,718 MT and 50,251 MT, respectively. Alfalfa hay exports to Canada dove 59% from more than 85,000 MT in 2024 to roughly 34,000 MT in 2025.

Other hay on the decline

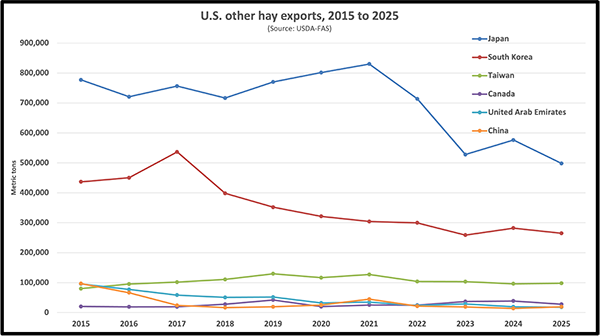

Hay exports other than alfalfa (mostly grass) totaled 952,663 MT in 2025. According to USDA-FAS data, this was down almost 10% year-over-year.

Japan remained the top export market for U.S. grass hay, receiving 498,303 MT. However, this was almost 14% less than the previous year. Japan’s buying power has been limited by the strength of the U.S. dollar compared to the Japanese yen. The challenging exchange rate has curtailed grass hay exports to Japan for the past several years, especially as other hay-producing countries become more competitive in the global market.

Grass hay exports to South Korea were down roughly 6% year-over-year at 264,723 MT. With that said, there was an uptick in grass hay leaving U.S. ports for South Korea toward the end of the year as the Asian country experienced its own poor forage harvest season. An outbreak of swine flu in Spain also narrowed South Korea’s hay buying options.

Taiwan followed in third place on leaderboard with 98,001 MT, which was relatively flat year-over-year. Canada’s demand for U.S. grass hay dropped 31% year-over-year for an annual total of 27,763 MT. Grass hay exports to the United Arab Emirates and China were 18,159 MT and 19,264 MT, respectively.

Summary

It was a tough year for U.S. hay exports in 2025, with totals for both alfalfa and grass hay exports taking big hits. Demand from our nation’s greatest alfalfa and grass hay customers — China and Japan — was much lower than the previous year, accounting for the lion’s share of the downward trend. Weakening dairy industries, trade disputes and tariffs, challenging exchange rates, and changing demographics in China and Japan are all factors for the declines.

For the first time since 2020, total hay exports to Japan surpassed those to China, even though the two countries both imported less alfalfa and grass hay year-over-year. This goes to show how great of an impact China’s deteriorating demand for U.S. alfalfa has on our nation’s hay export market as a whole.

Hay exports have a much stronger impact on Western hay production and market prices compared to the rest of the U.S., and last year’s situation will leave a noticeable bruise on Western growers’ bottom lines. In last week’s The Hoyt Report, author Josh Callen noted all hay exports out of the West Coast were down 11% year-over-year and fell below 3 million MT for the first time since 2016.

With that said, Callen pointed out that grass straw was a bright spot in the hay export market, with total straw exports exceeding 80,000 MT during the last three months of 2025. Less traditional straw products, such as ryegrass and bermudagrass straw, were on the rise. “While volumes for these products are a small part of the market, they were up sharply year-over-year,” Callen wrote.